Maximum drawdown with DCA

Maximum drawdown with DCA

Maximum drawdown with DCA

The article, part of our “Configuration of Investment Strategies” series, introduces the concept of Maximum Drawdown Money as applied within our StockPicker configurator.

In this article we are using a setting that was before deactivated, we set “Invest every rebalance = 1000”

In this way, we implemented a Dollar-Cost Averaging (DCA) strategy on top of our existing strategies and benchmarks.

But what exactly is DCA?

Dollar-cost averaging (DCA) is a prudent investment approach where a fixed sum, like $1,000, is consistently invested at regular intervals, typically on a monthly basis. This strategy is designed to mitigate the impact of market volatility by acquiring more shares when prices are low and fewer when prices are high. The test we’re presenting involves investing $1,000 each month, providing a visual representation of how DCA can influence investment performance and risk. The overarching goal here is to offer a more stable investment experience and potentially boost returns over time. As we’ll soon discover, our portfolio’s volatility is substantially reduced.

This strategy is often recommended for risk-averse individuals. Instead of deploying all their funds in a single lump sum, they can invest their money over the course of their investment horizon, thus minimizing potential market entry risk.

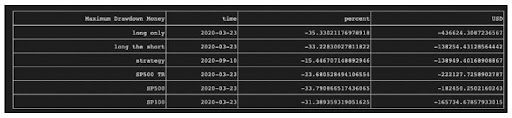

We can see the maximum drawdown of our strategies and benchmark while using DCA in the table Maximum Drawdown Money (supplementary indicator to the Maximum Drawdown Percentage).

You may notice similarities to the table in our previous newsletter, with one subtle distinction.

When we consider the compound interest generated by our investments, we find that the sum of money we’ll have at the end of the investment period significantly surpasses the initial amount. Consequently, the impact of drawdowns becomes more pronounced as we progress on our investment journey.

For example, if the market experiences a drop shortly after we initiate our investments, the “Drawdown Money” remains relatively modest due to the limited funds in our account.

Conversely, if the market undergoes a decline toward the conclusion of the testing period, the “Drawdown Money” takes on greater significance.

Table explanation

This is accounted for in the table, in fact in the column “percentage” we compare the percentage drawdown compared to the final value of the portfolio. In the column “USD” we can see the absolute value.

Now, thanks to the table, we can evaluate how our strategies + DCA performed compared to the benchmarks. First, let’s examine the performance of the “Long Only Strategy.” The maximum money drawdown observed was -35% during the 2020 crisis (compared to the max. percentage drawdown in 2008/2009). This level of volatility is expected for this strategy, as it is our most aggressive one. High volatility is anticipated and is typically rewarded with higher returns. Nevertheless, the drawdown of this strategy was comparable to that of the market, where the maximum drawdown for the S&P 100 was -33%.

Moving on to the “Long the Short Strategy,” as discussed previously, this strategy tests our model’s ability to identify underperforming stocks. The maximum drawdown for this strategy was -33%.

In the third row, we observe the Drawdown performance of our “Strategy.” This strategy maintains long positions in the top-performing stocks (those in “Long Only”) while simultaneously shorting the poorest-performing ones (those in “Long the Short”). Consequently, it maintains low volatility even during crises. For instance, during the 2020 crisis, our strategy had a maximum drawdown of only -15%, compared to the market’s drawdown of -31%.

In addition to percentages, it is possible to view the drawdown entity in absolute USD figures for both our strategies and the three benchmarks.